Auto, Pharma, IT, and Exports Drive India’s Leading State Economy

Key Highlights:

-

Maharashtra could hit $1 trillion GDP by 2030 – Morgan Stanley

-

Current GDP: $536B, India’s largest state economy

-

Services dominate at 64.3%, led by IT and finance

-

Attracted $19.6B FDI in FY25 – top in India

-

Major contributor to auto, pharma, exports

-

730 GCCs make it India’s Global Capability Centre hub

-

Strong fiscal health, low debt-to-GDP at 18.5%

In its report titled “Maharashtra – Leading the Way”, global investment bank Morgan Stanley says Maharashtra is on track to become a $1 trillion economy by 2030.

The state’s current GDP is around $536 billion, which is equal to Singapore’s economy. It is India’s largest state economy, accounting for 13.7% of the country’s total GDP.

The report attributes this sustained economic expansion to a mix of fiscal discipline, infrastructure investments, industrial growth, and inclusive social policies.

A Shift from Agrarian to Industrial Powerhouse

Maharashtra’s fiscal discipline has been central to its economic growth. As highlighted in the Morgan Stanley report,

“Fiscal prudence is evident with a debt-to-GDP ratio among India’s lowest. Even with a lower share of farm in output than the country’s average, it is India’s leading producer of several farm products.”

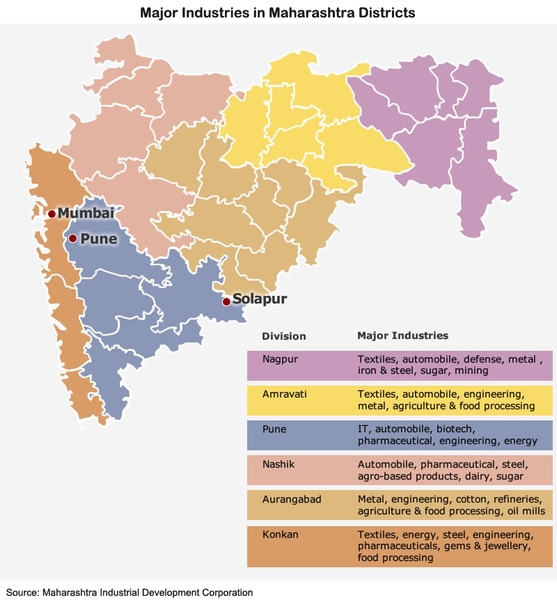

Building on this foundation, Maharashtra’s transformation from an agrarian state to an industrial and services-led powerhouse has driven its rapid ascent. Today, industrialisation accounts for 22.5% of the state’s GDP, anchored by core sectors like automobiles, metals, pharmaceuticals, and refined petroleum.

-

Maharashtra contributes:

-

20% of India’s total auto and auto parts output

-

16–17% in medicine and health equipment

-

8–12% in textile production

-

Yet, over the past decade, the share of industrial sectors in GDP has declined by 7.8%, while services surged by 9.2%, reflecting the broader economic shift.

Services Sector Dominates

Today, 64.3% of Maharashtra’s GDP comes from the services sector. The state has emerged as a key hub for IT, finance, real estate, insurance, and startups. It houses 730 Global Capability Centres (GCCs) as of FY24, making up 43% of India’s total GCCs, the highest in the country.

Maharashtra leads the country in attracting Foreign Direct Investment (FDI), securing $19.6 billion in FY25—39.2% of India’s total inflows. The state’s open investment policies, robust infrastructure, and business-friendly governance have helped it consistently remain a top choice for global investors.

Exports and Infrastructure Push

Maharashtra is India’s second-largest exporter after Gujarat, contributing 15.4% of the country’s total exports and accounting for 13.7% of the state’s GDP. Key export sectors include:

-

Jewellery

-

Electronics

-

Engineering goods

-

Pharmaceuticals

-

Chemicals

Major infrastructure projects like the Mumbai Trans Harbour Link, Navi Mumbai International Airport, and Vadhavan Port are expected to further boost trade and economic activity in the years ahead.

The Morgan Stanley report praises Maharashtra for its fiscal prudence. The debt-to-GDP ratio stands at just 18.5%, among the lowest in India, while the fiscal deficit has been kept under 3%, even during pandemic years.

Social indicators, such as literacy, gender parity, and regional equity, are improving. At the same time, the state is spearheading forward-looking initiatives like the MahaAgri-AI Policy 2025–2029, aimed at integrating AI into agriculture for better productivity and sustainability.

Challenges Ahead

While Maharashtra’s economic foundation is strong, the report warns against complacency. Challenges include:

-

Urbanisation stress

-

Manufacturing slowdowns

-

Agricultural income disparity

-

Climate-resilient development needs

To sustain its growth momentum, the state must continue innovating while addressing inequality and infrastructure gaps.

Maharashtra’s progress is vital to India’s $10.6 trillion vision by 2035. With strong leadership and focused strategy, the state isn’t just contributing—it’s leading the way.